Maxinvest

IT Services

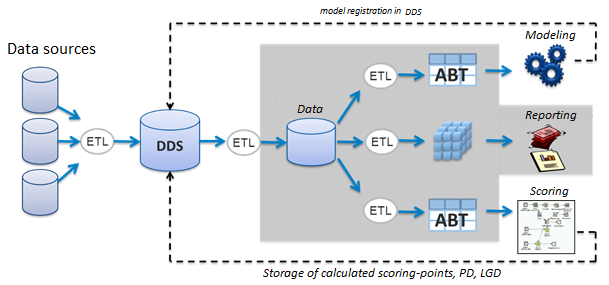

Data source / Registration of the model in DDS / Modeling / Reporting / Scoring / Data marts

Storage of accounting scoring scores, PD, LGD

ADVANTAGES OF SCORING SERVICE:

- Fast deployment and integration (within 10 business days)

- Integration with your IT environment

- The service is developed by Maxinvest data analysis specialists, that is already a guarantee of quality

- Low cost

FOR A WHAT?

For a qualitative assessment of credit risk (fraud prevention, proof of solvency and payment discipline).

To reduce costs (by reducing the number of personnel involved in the loan granting procedures)

To reduce the processing time for applications for loans (credit decision making is reduced for a few minutes)

To minimize operational risk

To analyze the reasons for low scoring assessment, and, accordingly, refusal to provide a loan (in cases of refusal)

Scoring in common with credit reports and verification of the borrower will allow you to build an effective system for making lending decisions.

FOR WHOM?

for banks

for credit unions

insurance companies

financial companies

mobile operators and telecommunications companies

other financial market participants entering into credit relations

Users can be banks, non-bank financial institutions, and other business entities that provide services with deferred payments, or provide property on credit.

A complete solution of the problem of credit scoring for banks, including functionality to support all the necessary processes. The solution includes tools for processing and storing information, building data marts, a wide range of analytical tools for building and analyzing credit scoring models and an extensive reporting system for solving the problems of assessing the performance of scoring models and the state of the loan portfolio.

The Maxinvest tools allow a data mining expert to create credit scoring models for consumer loans, credit cards, overdrafts, automotive, mortgage and other credit products. The scoring is aimed at solving various problems from assessing the probability of a client’s default to defining the strategy of the collection unit and creating a generally accepted rating model.